This is a complete guide comparing a DSCR loan vs. conventional loan.

Learn how to get the highest leverage with competitive interest rates.

Without destroying your credit score by applying to the wrong places.

Introduction to DSCR Loans and Conventional Loans

Both DSCR (Debt Service Coverage Ratio) loans and conventional loans are used by real estate investors. While conventional loans are widely recognized by both investors and regular homebuyers, DSCR loans are specifically designed for real estate investors.

Understanding the true differences for each, allows you to take advantage of both at the right time. Each loan type has its own eligibility criteria, benefits, and limitations. Both loan types can be an excellent choice for the same real estate investor, but at different times of their investment journey.

Who Can Benefit?

DSCR Loans: Ideal for real estate investors focused on rental or commercial properties. These loans allow borrowers to qualify based on property income rather than personal income. Offering flexibility for the self-employed, individuals with variable income streams or real estate investors that write everything off (you know who you are).

Conventional Loans: Best suited for homebuyers, individuals purchasing second homes or investors with high income who don’t use tax advantages. These loans have strict guidelines and rely on the borrower’s creditworthiness, annual income, tax returns and debt-to-income ratio.

Let’s explore each loan type in more detail.

What is a DSCR Loan

A DSCR loan is specifically designed for investment property investors or landlords. DSCR loan lenders approve or deny loans based on the income generated by the property rather than the borrower’s personal finances. These asset based loans use a DSCR ratio, appraisal value and local monthly rental rates to determine a loan amount and interest rate.

Definition of DSCR

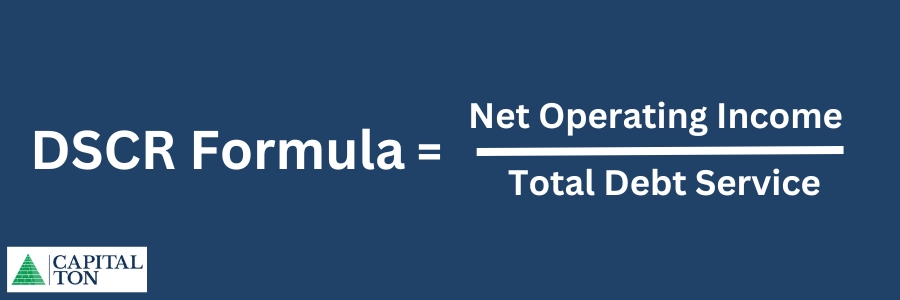

The Debt Service Coverage Ratio (DSCR) is the most important metric that lenders use to determine whether a property’s cash flow is sufficient to cover its monthly debt payments (principle, interest, property taxes and insurance).

Here’s the official DSCR formula:

Net Operating Income (NOI): Monthly rental income generated by the subject property. When purchasing a rental property, the projected monthly rent will be calculated on the appraisal. When refinancing, DSCR loan lenders will typically use the stated rental income, local monthly rent calculated on the appraisal or an AirDNA analysis for short term rentals.

Total Debt Service: The sum monthly loan payments (principal and interest), property taxes, landlord insurance and any HOA fees.

Example of DSCR Calculation

Here’s an example of a DSCR loan in Florida. Let’s say a rental property is $393,698 and the projected rental income is $4,000 per month. Since, Florida’s effective property tax rate is 0.80%, we can estimate an annual property tax of $3,149 and average landlord insurance of $2,000.

Using today’s current interest rates at 7% (example), the monthly loan payment would be $2,095, assuming a standard 20% down payment and 80% LTV. After reducing the annual property taxes and landlord insurance to a monthly amount, we get:

DSCR Calculation = $4,000 / ($2095 + $262 + $166)

DSCR Ratio: 1.58

A DSCR of 1.58 means the property generates 58% more income than is needed to cover its monthly debt obligation. DSCR lenders typically require at least a 1.0 DSCR, use our DSCR calculator to see if you qualify.

Benefits of DSCR Loans

Asset Based Approval

Unlike traditional loans, DSCR loans don’t require personal income verification. Therefore approval is based on the property’s ability to generate an income, the appraisal value and projected monthly rent. Focusing on property income makes the approval process quicker and less complicated.

Flexible Loan Terms

Since approval is based on the DSCR ratio, properly manipulating it is key to getting approved. For example, a good DSCR loan lender will educate you on lowering your loan amount to reduce your monthly payment. They may also ask you to shop around for a lower insurance quote or buy down your interest rate with points.

No Income Verification

Borrowers aren’t required to submit 2 years of tax returns or verify their current personal income. This is excellent for self-employed individual who run a business, freelance or use many tax advantages such as depreciation.

Fast Closing Process

Since DSCR loans ask for minimal documentation, they can close much faster than conventional loans. When comparing a DSCR loan vs conventional loan, the average time for a DSCR loan is 22-24 days. Which is faster than the typical 45-60 day close for a conventional loan.

Faster Rental Portfolio Growth

Since approval is based on the property and not personal finances, borrowers can finance multiple properties, allowing for faster rental portfolio expansion. With conventional financing, every additional rental property purchase adds more monthly debt to your credit report. With depreciation and monthly expenses that are reported on tax returns, buying another rental property becomes very difficult.

Credit Score Flexibility

While DSCR loans typically require a 680 or higher credit score, you can still get approved with a 620 or higher by meeting a higher DSCR requirement.

Limitations of DSCR Loans

Higher Interest Rates

Since DSCR loans are offered by private money lenders, they typically come with slightly higher interest rates.

Higher Down Payments

Borrowers typically have to put a down payment of 20% or more. Sometimes the local monthly rent trends aren’t favorable, so borrowers have to reduce leverage to meet the minimum DSCR requirements. Lowering leverage, comes with a higher down payment.

Limited Availability

99% of traditional banks and credit unions do not offer DSCR loans and most hard money lending companies do not specialize in DSCR loans.

What is a Conventional Loan

A conventional loan is a standard mortgage that is offered by a traditional bank. These loans are often used to buy primary residences, second homes, or investment properties. A conventional loan follows strict guidelines set by Fannie Mae and Freddie Mac, the two major organizations that regulate most mortgage guidelines.

Debt-to-Income Ratio

One of the most important factors when qualifying for a conventional loan is the borrower’s debt-to-income ratio (DTI). This ratio measures how much of your personal income goes toward monthly debt payments, such as monthly mortgage payments, car payments, credit card payments, and other loan payments. This indicates your financial stability to a mortgage lender.

DTI Formula

(Total Monthly Debt Payments / Gross Monthly Income) × 100

Example of DTI Calculation

Let’s say your gross monthly income is $6,000 and your monthly debt payments total is $2,000. Assuming these numbers, your DTI would be:

DTI = ($2,000 / $6,000) × 100 = 33.33%

Most banks prefer borrowers with a DTI below 43%, although some may accept higher ratios under certain circumstances.

Benefits of Conventional Loans

Lower Interest Rates

Conventional loans generally have lower interest rates than DSCR loans, making them more affordable in the long term. Borrowers with strong credit history can access competitive interest rates.

Property Versatility

Conventional loans can be used to finance primary residences, second homes, and investment properties.

Private Mortgage Insurance

If you put down less than 20%, private mortgage insurance (PMI) is required. However, but it can be removed once you reach 20% equity. Using PMI allows you to buy real estate with a lower down payment.

Lower Down Payment

Assuming your personal income allows an additional real estate purchase, it is possible to buy real estate with a 20% down payment or even 3% down payment by using PMI.

Widely Available

Any mortgage broker can offer a conventional loan, giving you plenty of financing options.

Limitations of Conventional Loans

Strict Loan Requirements

When comparing a DSCR loan vs conventional loan, these type of loans have strict qualification guidelines. Lenders will require a high credit score, low debt to income ratio, and 2 years of consistent income to qualify.

Slow Approval Process

Typical loan documentation requires 2 years of personal tax returns, pay stubs, 24 months of bank statements, a comprehensive credit report, background check, employment verification and more.

Slow Closing Process

Due to strict guidelines in the mortgage industry, extensive documentation and verifications, it usually takes 45-60 days to close.

Loan Limits

Conventional loans are subject to conforming loan limits, which vary by location and may work for high-value properties.

Differences Between a DSCR Loan vs Conventional Loan

Purpose

DSCR Loans: Specifically designed for real estate investors to finance investment properties using rental income.

Conventional Loans: Broadly used for primary residences, second homes, and investment properties.

Approval Criteria

DSCR Loans: Approval is based on the subject property’s income, not the borrower’s personal finances.

Conventional Loans: Approval depends on the borrower’s financial stability, such as the total reoccurring monthly debt, car payments, primary residence payments, pay stubs, etc.

Loan Terms

DSCR Loans: Flexible loan terms and approval guidelines designed for real estate investors.

Conventional Loans: Standardized terms set by federal government guidelines.

Down Payment

DSCR Loans: Require larger down payments, often 20% or more.

Conventional Loans: While a standard down payment is 20% or more, PMI insurance can be used for a 3% down payment for qualified borrowers.

Interest Rates

DSCR Loans: Slightly higher rates due to increased risk for private lenders. Typically 0.5%-1% compared to traditional banks.

Conventional Loans: Lower rates tied to borrower credit scores.

Closing Speed

DSCR Loans: Fast closing process due to less documentation.

Conventional Loans: Slower closing due to extensive documentation and verification.

Similarities Between a DSCR Loan vs Conventional Loan

Despite their differences, these loans share some similarities:

Property as Collateral

Both loans use the property as collateral, meaning the lender can assume the property if on-time payments are not made.

Long-Term Financing

Both loan types are used for long-term financing, with 10, 15 or 30 year loan terms.

Loan Approval

Loan approval is based on the property’s purchase price, appraisal value and a properly submitted loan application.

What Loan Type is Right For You?

When deciding between a DSCR loan vs conventional loan, consider this:

- Is your personal income sufficient to cover an additional real estate purchase?

- Do you have any red flags on 24 months of your bank statements?

DSCR Loans

Real Estate Investors: Particularly those who use tax deductions, tax advantages and who want to grow a rental portfolio.

Self-Employed Borrowers: Those with inconsistent income.

Time-Sensitive Borrowers: Investors who need a fast closing.

Conventional Loans

Homebuyers: Individuals purchasing primary residences or second homes.

Stable Income Earners: Borrowers with strong credit, low DTI, and stable income.

Cost-Conscious Borrowers: Those looking for lower interest rates and minimal closing costs.

How to Get High Leverage and Low Interest Rates

If you qualify for PMI insurance with a traditional bank, you can put down as low as a 3% down payment with a conventional mortgage. However, if you don’t want to deal with 2 years of personal income verification, a DSCR loan is right for you.

You can get high leverage and low interest rates by either finding real estate that’s undervalued, finding a property that generates current cash flow compared to its monthly debt obligations, shop around for a lower insurance quote or buy down interest rate with points.

How to Improve Loan Eligibility

Tips for Both Loan Types

- Build credit by paying bills on time, reduce debt, and check for errors on your credit report.

- Put down a larger down payment to improve your chances of approval.

Tips For DSCR Loans

- Shop around for the lowest insurance premiums.

- Renovate the property, to increase the appraised value before refinancing and to adjust rent to match rental market rates.

- Buy down interest rates with points.

Tips For Conventional Loans

- Pay off existing debts

- Find ways to increase your income

- Work with a financial advisor